Around 47 % of homes in the United States have some sort of mold or dampness, which creates thousands of home insurance mold claims annually. However, despite this alarming figure, most property owners discover too late that most standard policies don’t automatically offer mold damage coverage.

Whether homeowners’ insurance covers mold depends entirely on the cause, timing, and your policy’s terms. Here’s everything you need to know about it:

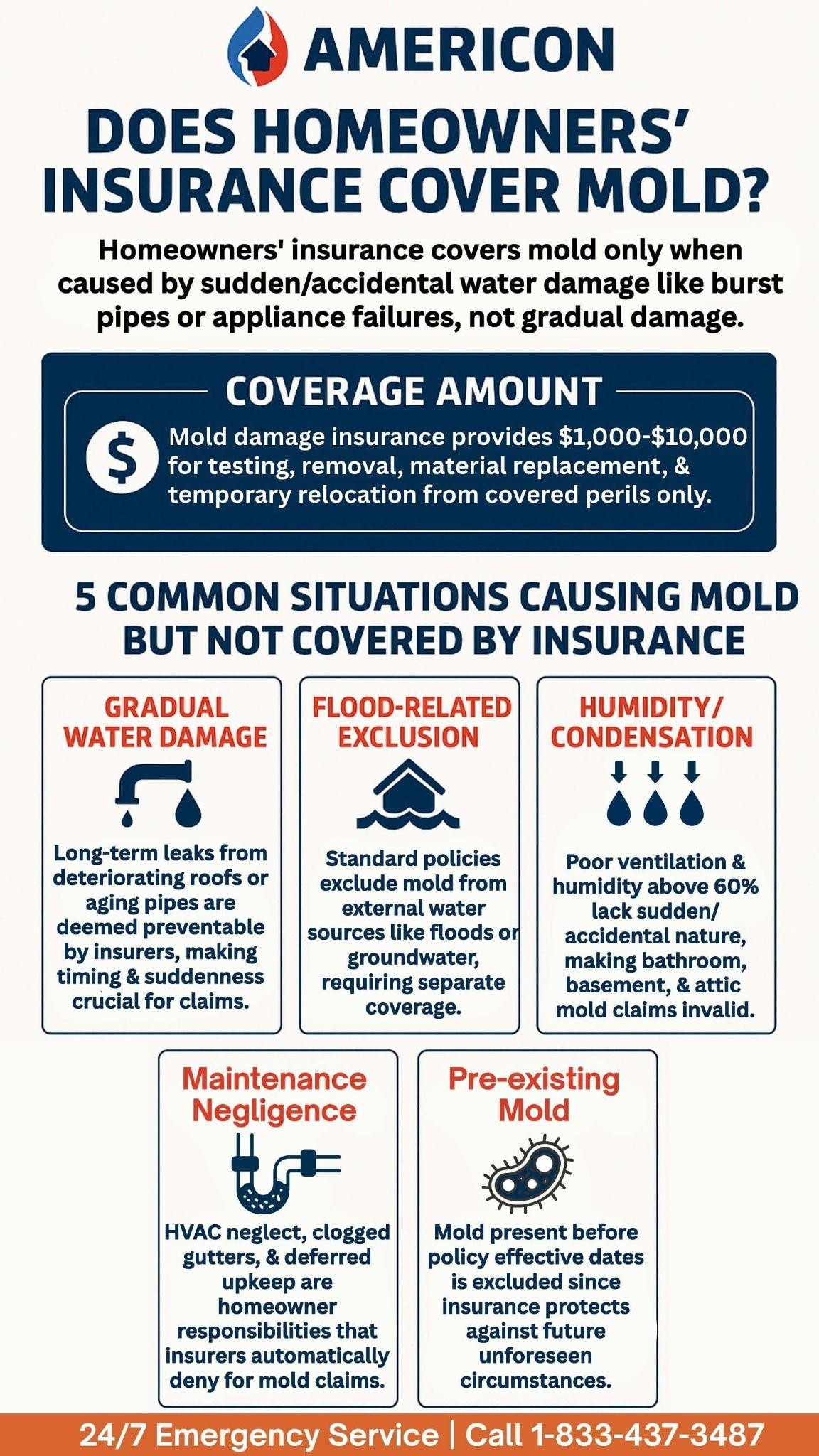

Does Homeowners’ Insurance Cover Mold?

No, homeowners’ insurance doesn’t typically cover mold damage unless it’s a direct result of a covered peril. Mold damage insurance is only offered when the damage stems from sudden or accidental water damage.

This includes situations such as:

- Burst water pipes causing immediate flooding and water damage

- Appliance hose failures, such as washing machines

How Much Does Insurance for Mold Damage Cover?

While most homeowners’ insurance policies cover sudden and accidental water damage, it’s only limited to $1,000 to $10,000. This coverage only applies to covered perils, such as:

- Mold testing and inspection

- Mold removal and remediation services

- Replacement or reconstruction of damaged areas

- Temporary relocation expenses

5 Common Situations Causing Mold But Not Covered by Insurance

1. Gradual Water Damage

Long-term leaks from dilapidated roofs or aging pipes that result in mold are considered preventable by insurance companies, which is why they’re not covered in mold remediation insurance. The key distinction here is timing and cause.

2. Flood-Related Mold Growth

Standard insurance policies, unfortunately, don’t cover mold growth that’s been caused by water from external sources such as floods or groundwater. While this results in a significant coverage gap, having a flood insurance policy is always helpful, especially if you live in areas where floods are frequent.

3. High Humidity or Condensation

Since mold growth from poor or inadequate ventilation lacks the sudden, accidental nature, it’s not valid for a home insurance mold claim. While humidity is an environmental factor, it’s considered controllable by maintaining indoor humidity levels below 60% with the help of a dehumidifier.

Common areas that are subject to humidity-related mold growth include:

- Bathrooms

- Basements

- Attics

- Crawl spaces

4. Maintenance-Related Issues

A neglected HVAC system or clogged gutters, among other maintenance-related issues, are not covered by a homeowner’s insurance policy. Since regular maintenance is considered the homeowner’s fundamental responsibility, lack of maintenance is denied by all insurance companies.

5. Pre-existing Mold Issues

Mold found before your insurance policy’s effective date is automatically excluded from coverage. This is because insurance is designed to protect homeowners from future, unforeseen circumstances rather than solving existing problems.

This means that homeowners’ insurance policy usually covers mold on a case-by-case basis. Insurance companies will typically request proof that the mold developed after the effective date and resulted from a covered peril.

How to File an Insurance Mold Claim

1. Document Everything Immediately

Make sure to make a record of everything. This includes taking extensive photos and videos of the mold, the source of water damage, such as flood or water accumulation from firefighting efforts, and other affected areas. It would also help to create a timeline of when you discovered the problem and what immediate actions were taken.

2. Contact Your Insurance Company

When reporting a claim, time is of the essence, and you typically have under 48 hours to do it. Delaying this can result in claim denials, especially if the insurance company believes that immediate action could have prevented additional damage.

3. Get a Professional Assessment

While documenting all mold damage on your own is encouraged, professional reports often hold more weight than homeowner assessments.

4. Keep Detailed Records

Throughout the claims process, make sure to save all receipts for emergency repairs, temporary accommodations, and other professional services you may have hired. It’s also worth documenting phone calls, emails, and any correspondence with your insurance company so you can go back to them when needed.

5. Follow Mitigation Requirements

Most insurance policies require homeowners to take necessary and immediate steps to prevent further damage. This could include stopping the leaking water source, removing standing water, and beginning to dry the affected area.

What Other Coverage Options Do You Have?

Since a homeowner’s insurance policy offers limited protection from mold damage, here are some other options that are worth having a look at:

1. Concealed Water Damage

A few insurance companies may offer this as an optional add-on for covering mold damage that is a result of a hidden leak. This includes hidden areas such as behind walls and under floors, where homeowners may not be able to detect problems immediately.

2. Water Backup Coverage

A water backup coverage is again an add-on and may offer coverage for mold that resulted from sewage backup.

3. Flood Insurance

As mentioned earlier, flood insurance is useful for mold damage that is a result of a flood.

Here are some important things to keep in mind:

- Flood insurance must be purchased separately from a homeowner’s insurance

- There is usually a 30-day wait period before the insurance takes effect

- Time limits, typically 48 hours, apply for reporting and addressing mold after flood damage

How Much Does Mold Remediation Cost Without Insurance Coverage?

Most homeowners pay anywhere between $1,500 to $9,000 for mold remediation, with an average cost of $3,500.

| Area | Average Cost Range

|

| Attic

|

$1,000 to $9,000 |

| Basement

|

$500 to $4,000 |

| Bathroom

|

$500 to $1,500 |

| Crawl Space

|

$500 to $2,000 |

Factors that can affect mold remediation costs:

- The type of mold and the toxicity level

- How accessible the affected area is

- The extent of the structural damage

- Labor costs

- Material costs

How to Prevent Mold in Your Home

Insurance claims for mold damage can be tricky. This is why prevention is always recommended. Some useful tips include:

- Check for leaky faucets around your home and make repairs right away

- Inspect your basement, attic, or crawl spaces for moisture or musty smells

- Maintain indoor humidity levels between 30% – 50% through proper ventilation

- Watch out for and address condensation issues around walls and windows promptly

- Install exhaust fans in areas where adequate ventilation might be a problem

- Clean out your gutters and keep them functional

Americon Restoration Helps With Insurance Claims Assistance:

Besides being a professional decontamination and mold remediation company in Ohio and Pennsylvania, we also help our clients with documentation, adjuster communication, insurer negotiations and other aspects of insurance claims so that you have a full peace of mind knowing experts are handling every part of the restoration from the actual work to getting you paid. Call us at 1-833-437-3487 to get started asap.

Frequently Asked Questions:

Mold tests are usually not covered by standard homeowners insurance unless the mold resulted from a covered peril, such as water damage from a burst pipe. Coverage depends on the policy’s specific terms and exclusions.

Home warranties do not typically cover mold remediation. Mold is generally considered a result of poor maintenance or environmental conditions, which are excluded under most home warranty plans.

The mold exclusion in insurance policies refers to a clause that denies coverage for mold damage unless it is directly caused by a covered peril. This exclusion limits claims related to mold from humidity, flooding, or poor maintenance.